The Bankers' Bluff on Savings and Private Pensions

Having read yet another wise vision from G. Rungainis (Prudentia) on the future of state pensions - namely that in future the state will only be able to provide accommodation in a social-type home and a minimal daily allowance - as well as the similar opinions of several other bankers or ex-bankers glorifying private savings, an irresistible desire arose to put the numbers on paper and draw one's own conclusions.

Having read yet another wise vision from G. Rungainis (Prudentia) on the future of state pensions - namely that in future the state will only be able to provide accommodation in a social-type home and a minimal daily allowance - as well as the similar opinions and positions of several other bankers or ex-bankers glorifying private savings, an irresistible desire arose to put the numbers on paper and draw one's own conclusions.

The Bank Lobby

In reality, concerns about the usefulness of savings were prompted by the following circumstances - the constantly rising food prices and the slow but nonetheless rising both minimum wage and average wage across sectors. The second is the special status of banks and the world economy both within the state system and in each of our daily lives. This is demonstrated both by the publicly reported progress of the Parex Bank rescue - namely, that the decision to pour virtually all the money in the country down the throat of one private bank can be taken by a very small number of people - and by the state's unhealthy desire to peer into its residents' "bedroom" and either force money to be kept in banks or even lay claim to a portion of it. The latter, hiding behind the noble banner of combating corruption, looks very much like the bank lobby. It may be that the political gain compared with the "minor" costs related to account servicing and transaction commissions is considerably greater. Be that as it may, a commission of 0.30 Ls is equivalent to purchasing 1 kg of potatoes, which, turn it however you like, is enough for one meal for a family with two children.

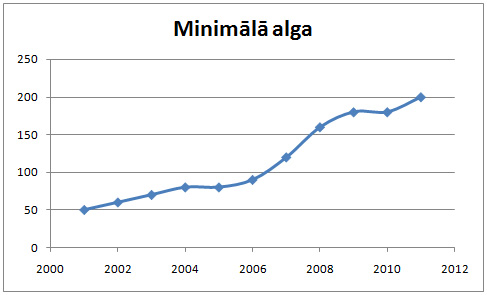

Changes in Minimum Wage by Year

|

2001 |

2002 |

2003 |

2004 |

2005 |

2006 |

2007 |

2008 |

2009 |

2010 |

2011 |

|

50 |

60 |

70 |

80 |

80 |

90 |

120 |

160 |

180 |

180 |

200 |

Minimum wage growth by year. According to csb.lv data

The fact that the minimum wage in many sectors is also the actual wage is a well-known fact. The diagram shows that over 10 years the wage has grown from 50 Ls to 200 Ls, i.e. it grew on average by 15% per year.

Question 1. Which bank is able to offer deposit interest of 15%?

The numbers can also be looked at differently: knowing that the minimum wage grows by 15% each year, each year we deposit 1 month's salary in the bank (without interest). As a result, saving for 10 years we will have saved enough to cover only 6 months in the 11th year.

If during a lifetime a person works from age 25 to 65, depositing one month's salary each year, then after 40 years of work experience the savings will be sufficient to last without worry for another 20 years. Sounds good, if only one knew for certain that one would live only until age 85…

That was the good news. The bad news is that not only wages grow, but also food and service prices.

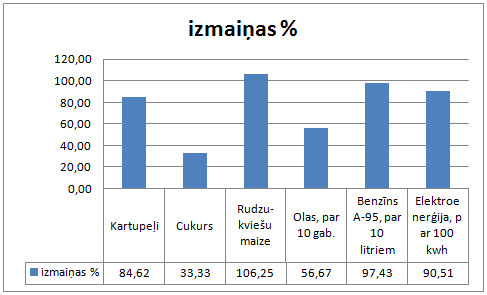

Food and Service Prices

|

Product |

2000 |

2001 |

2002 |

2003 |

2004 |

2005 |

2006 |

2007 |

2008 |

2009 |

2010 |

|

Potatoes |

0,13 |

0,14 |

0,23 |

0,17 |

0,17 |

0,2 |

0,3 |

0,36 |

0,32 |

0,29 |

0,24 |

|

Sugar |

0,48 |

0,5 |

0,54 |

0,56 |

0,65 |

0,66 |

0,68 |

0,75 |

0,74 |

0,71 |

0,64 |

|

Rye-wheat bread |

0,32 |

0,3 |

0,31 |

0,3 |

0,31 |

0,34 |

0,39 |

0,49 |

0,67 |

0,7 |

0,66 |

|

Eggs, per 10 pcs. |

0,6 |

0,61 |

0,54 |

0,59 |

0,61 |

0,6 |

0,64 |

0,74 |

0,93 |

0,96 |

0,94 |

|

Petrol A-95, per 10 litres |

3,89 |

3,83 |

3,78 |

4,02 |

4,52 |

5,58 |

6,01 |

6,3 |

7,13 |

6,72 |

7,68 |

|

Electricity, per 100 kWh |

3,9 |

3,9 |

3,9 |

3,9 |

4,5 |

4,5 |

4,75 |

5,1 |

6,6 |

7,43 |

7,43 |

Changes in product and service prices over 10 years. According to csb.lv data

As we can see from the table of food and other product prices, over 10 years prices have risen across all categories. The largest increase - rye bread (106%), fuel (97%), and electricity (90%). The average increase across all categories over 10 years - 78%, or ~8% per year.

Question 2 - which bank offers deposit growth of 8% per year? Although this figure already sounds closer to a realistic bank deposit interest offer, it is still far from the truth.

These numbers can also be looked at differently - after 40 years of work and carefully saved pension, with each passing year your saved sum will decrease by 8% per year. This in turn means that after 10 years (i.e. at age 75) you will have to realise that with your saved money you will be able to afford to buy only 20% of the range of goods you could have bought 10 years earlier.

Conclusions

- Banks crossed the red line long ago, namely by abandoning currency backing (with gold), which in turn means that the pace and volume of printing paper money is no longer determined by the state's availability of natural resources, but by the decision of a few people (with straighter or more crooked noses).

- A long-term money deposit is ineffective and absurd.

- Banks (and financial companies) and their clients are in unequal positions - financial speculation is not taxed, whereas wages and goods are.

- Although banks stand outside politics and the state, their importance and influence is as great as the influence of the church in the Middle Ages.

comments